Updated: November 9, 2025. This TrenBuzz explainer breaks down the headline idea that has been trending as the “Trump 50 year mortgage”: what a 50-year mortgage actually is, what the White House and housing regulators have said, the math behind longer terms, the legal and policy hurdles, who wins and who loses, and how to think about this if you’re shopping for a home. Read for a plain-English, step-by-step guide and a practical example you can use today.

Quick summary — Trump 50 year mortgage

The administration signaled it is working on enabling 50-year mortgages, a proposal tied to White House housing affordability goals and comments from the FHFA director confirming the idea is under active study. The proposal aims to lower monthly payments by stretching repayment, but it also slows equity building and can dramatically raise lifetime interest costs unless rates for longer terms remain very close to current 30-year rates.

1 — What is a 50-year mortgage, in plain terms?

A 50-year mortgage is a traditional fixed-rate home loan where the borrower repays principal and interest over 600 months instead of the more common 360 months (30 years).

Monthly payments are typically lower because the principal is spread over a longer period, but you pay interest for many more years and build home equity much more slowly. For basic mechanics and examples, consumer-finance explainers are a useful primer.

2 — What the White House / housing authorities have said (the recent headlines)

In early November 2025 the topic resurfaced after social posts attributed a 50-year mortgage push to the President and the Federal Housing Finance Agency (FHFA) director indicated the agency is “working on” options to broaden mortgage terms. The administration frames the change as a tool to improve affordability by lowering monthly payments for first-time and younger buyers.

3 — Why this idea is suddenly newsworthy (policy context)

The U.S. housing market has struggled with high rates, limited inventory, and declining affordability. Extending the standard loan term is an obvious, headline-friendly lever to reduce monthly outlays immediately — but it’s not a cure for supply shortages, and it raises trade-offs about long-term wealth building. The proposal sits alongside other housing moves the administration has discussed, including changes at Fannie Mae and Freddie Mac.

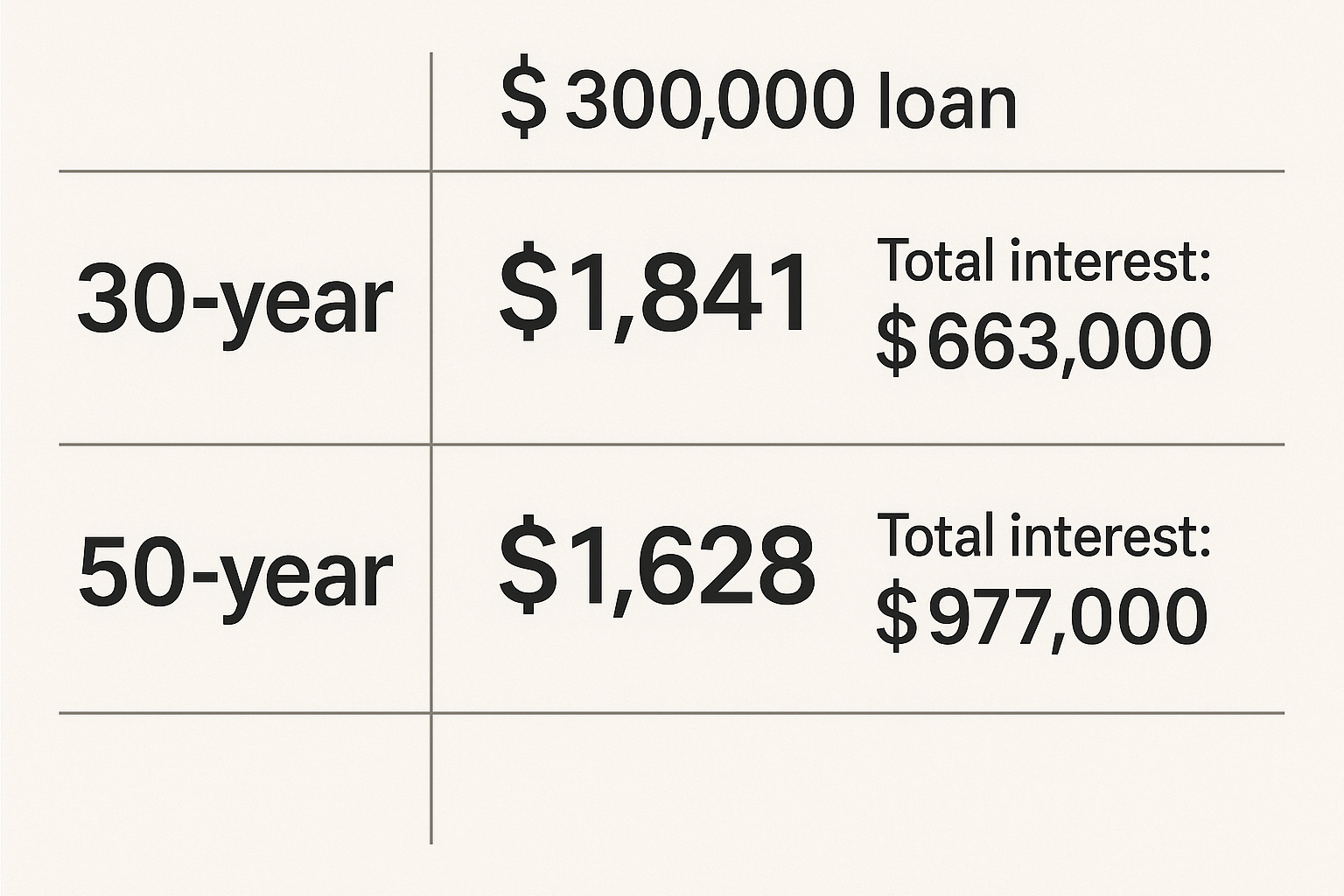

4 — The short math: monthly payment example (exact numbers)

Using a representative 30-year mortgage rate (30-yr fixed = 6.22% — Freddie Mac weekly average) as our baseline, here’s a clean comparison for a $300,000 loan:

• 30-year @ 6.22%: monthly payment ≈ $1,841.

• 50-year @ 6.22%: monthly payment ≈ $1,628.

That’s about $213 less per month on the same loan amount if the interest rate stayed identical — but see the next section on total cost.

Important arithmetic note: stretching the loan from 30 to 50 years lowers the monthly payment, but increases the number of months paying interest. At the identical rate above the borrower would pay roughly $314,000 more in interest over the life of the loan (50-year total paid ≈ $977k vs 30-year total ≈ $663k). Those are material differences. (I used typical market figures current in early November 2025 to show the scale of the trade-off.)

5 — Why the “savings” can be misleading: longer terms often cost more per month if rates rise

One common misread is to assume a longer term always reduces monthly out-of-pocket costs. In practice, lenders will typically charge a higher rate for longer maturities (term premium). If a 50-year rate is materially higher than a 30-year rate — even by 0.5%–1.0% — the monthly payment benefit can shrink or reverse. In one sensitivity example, a 50-year rate 1.0% higher than a 30-year rate produced a monthly payment slightly higher than the 30-year case. That math is why many analysts warn that payment reduction is not guaranteed.

6 — The policy and legal hurdles you should know about

Allowing a nationwide shift to 50-year terms at scale would involve regulatory changes and possibly congressional action. Some analysts note that certain post-2008 financial-regulation constraints (including elements of the Dodd-Frank architecture and underwriting standards) would have to be reexamined to ensure safety and soundness. Housing policy experts emphasize that lenders, the GSEs (Fannie/Freddie) and the FHFA would all play central roles; this is not an overnight switch.

7 — Who benefits — and who pays — in plain language

• Potential beneficiaries: younger buyers constrained by monthly payment windows; households wanting lower payments now to manage budget pressure.

• Downsides / parties that “pay”: long-term homeowners who build equity more slowly; borrowers who may pay far more interest over decades; the broader housing finance system (counterparty risk in mortgage pools), and future resale markets where owners may have less built-in equity. The distributional impacts are complex: upfront affordability vs lifetime wealth accumulation.

8 — How lenders and the secondary market (Fannie/Freddie) would be affected

Large mortgage buyers and guarantors need to price and manage duration risk. If GSEs back 50-year loans at scale, they must manage the longer interest-rate exposure and capital needs. The FHFA’s role is therefore central — the agency would shape whether Fannie/Freddie purchase such loans and under what guardrails. That is why the FHFA director’s comments matter and why industry watchers are closely reading agency signals.

9 — The equity and refinancing picture (practical follow-up)

Slower principal amortization means borrowers build equity more slowly. That affects the ability to refinance, tap home equity, or sell without needing a larger down payment later. It also changes how mortgage insurance and loan-to-value (LTV) calculations behave in years 5–10. For households planning to move frequently, a long term may be a poor match because they may not enjoy the lower payment window long enough to offset higher lifetime interest.

10 — Behavioral risks and unintended consequences

Longer mortgage terms can create moral-hazard or behavioral changes: people might buy pricier homes because monthly payments look affordable, which can push prices up and counteract the initial affordability goal. Another risk is that lower monthly payments might reduce urgency to refinance in falling-rate environments, locking borrowers into high cumulative interest through inertia. Policymakers must weigh these behavioral angles.

11 — How the proposal could be designed to reduce harm

Policy designers could add safeguards: higher underwriting standards, mandatory borrower counseling, caps on allowable loan-to-income ratios, or initial amortization schedules that front-load principal for the first years. Alternatively, targeted 50-year options could be limited to certain first-time buyers or set with maximum LTV limits to protect taxpayers and investors. Those are the kinds of guardrails many housing economists recommend when discussing longer terms.

12 — What you should do if you’re shopping for a home right now

- Don’t assume a 50-year product is the only way to lower payments — shop rates, consider adjustable-rate or buy-down strategies, or change loan size instead.

- Run the math for several scenarios: (a) same rate, longer term; (b) longer term with a rate premium; (c) refinance options down the road. The lifetime interest and equity timeline matter far more than a single-month saving.

- Plan your expected homeholding timeframe: if you expect to move in 5–7 years, very long terms often make less sense. If you plan to stay 25–30 years, compare long-term totals carefully.

- Talk to a mortgage professional who will show amortization schedules and explain closing costs and insurance impacts. These conversations matter for real financial outcomes.

13 — The politics and next steps — what to watch

Expect several near-term developments: administration statements clarifying eligibility or scope; FHFA technical papers on duration and risk; lender pilots or product proposals; and commentary from consumer groups and housing economists. Congressional oversight hearings or legislative proposals may follow if the administration moves to change legal constraints around mortgage terms. Keep an eye on official FHFA communications and Treasury/HUD briefings for concrete rule proposals.

Simple consumer example recap (one last look at the numbers)

If you like numbers, remember this simple rule: longer term = lower monthly payment but more interest paid overall unless the lender charges the same rate. At current market norms (30-yr average around 6.22% in early November 2025), a $300,000 50-yr loan at the same rate cuts the payment by about $213/month but increases the total paid by roughly $314,000 over the life of the loan. That tradeoff is the core of this debate.

50‑Year vs 30‑Year Mortgage Calculator

Sources & verification (key reporting and data used)

Major reporting and authoritative data used to prepare this explainer (checked Nov 9, 2025): recent news coverage of the administration’s 50-year mortgage discussion; FHFA director remarks; consumer finance explainers; and weekly mortgage rate data (used for the math examples).

TrenBuzz disclaimer

This article is an informational explainer based on public reporting and current mortgage-rate data as of November 2025. It is not financial or legal advice. For personalized mortgage calculations, tax implications, or to evaluate loan offers, consult a licensed mortgage professional or financial advisor.