Published by TrenBuzz.com | May 16, 2026

Key Points at a Glance – Practical Steps Americans Are Actually Using to Survive Gas Prices

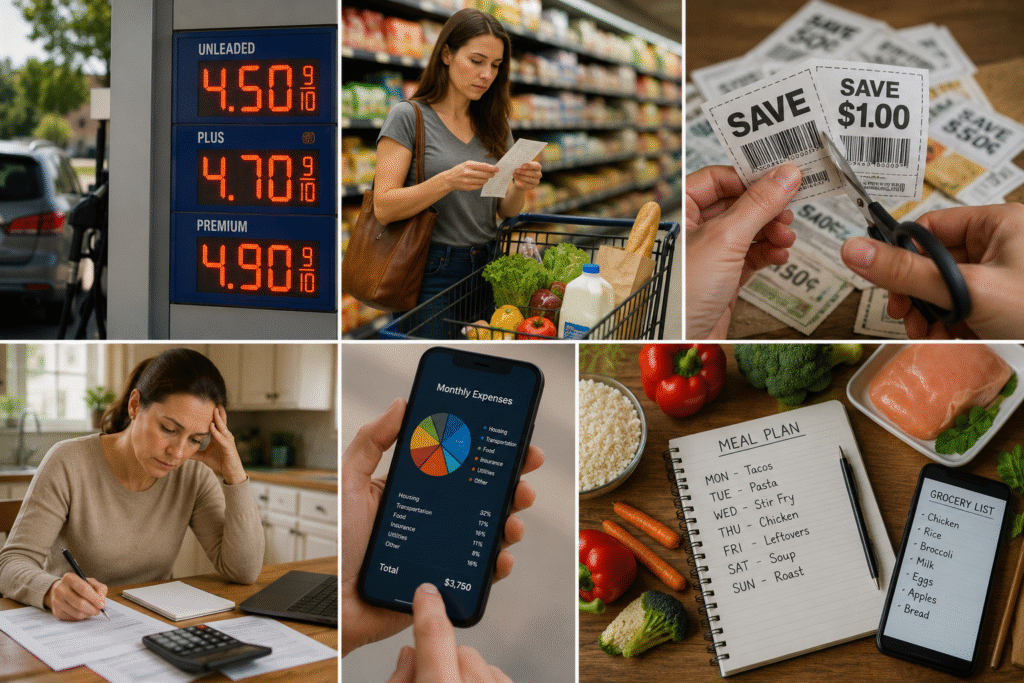

- National average gas price hit $4.50/gallon in May 2026 — up 51% since February 28 when the Iran war began.

- Diesel costs $5.64/gallon — pushing up prices on everything delivered by truck, which is almost everything.

- CPI inflation surged to 3.8% in April — the highest since May 2023 — with energy driving 40% of the increase.

- The average US household now spends $320+ per month on gas — up from $195 in late February.

- Grocery prices have risen 12% year-on-year — milk, eggs, and meat seeing the sharpest increases.

- A federal gas tax holiday (saving 18.4 cents/gallon) is being debated in Congress but not yet passed.

- The US average household has $7,951 in credit card debt — and debt loads are growing as people charge necessities.

- Financial experts recommend the 50/30/20 budget rule, but suggest adjusting to 60/20/20 during a crisis period.

- Carpooling, remote work requests, and grocery store brand switching are the top three cost-cutting behaviors among Americans right now.

- One key expert insight: “This is a temporary shock — protect your emergency fund now, before it gets worse.”

Nobody needs a chart to feel it. It’s there every time you pull up to a pump, scan your groceries, or open a credit card statement. The question isn’t whether prices are hurting — they are. The question is what you can actually do about it.

Understanding What’s Driving the Pain Right Now

The Iran war, which began February 28, has blocked roughly 20% of the world’s oil supply flowing through the Strait of Hormuz. That one fact is responsible for most of what you’re paying at the pump today.

Diesel at $5.64 doesn’t just hurt truckers — it raises the cost of delivering every product in America. Grocery stores, pharmacies, and retailers are all passing those logistics costs on to you, and they’re not rushing to reverse it even if diesel drops.

Step 1: Run a Real Budget — Not the One You’re Guessing At

Most Americans significantly underestimate how much their gas bill has risen since February. The jump from $2.98 to $4.50 per gallon sounds manageable until you multiply it across every fill-up of the month.

Pull your actual bank and credit card statements from February and compare them to May. The gap — across gas, groceries, and utilities — will be a number that clarifies everything and motivates action faster than any financial advice article can.

Step 2: Attack the Gas Bill First — It’s the Most Controllable

Carpooling even twice a week cuts your gas spending by roughly 30-40%. Apps like Waze Carpool and Rideshare 2.0 are seeing record signups in May 2026 — you’re not alone in looking for this option.

If your job allows it, request two work-from-home days per week. That single change can save the average American commuter $90-120 per month in fuel costs at current prices, with zero lifestyle sacrifice.

Use GasBuddy or your AAA app to find the cheapest gas within five miles. Price differences of 25-35 cents per gallon are common between stations in the same neighborhood right now — and that adds up to real savings over a month.

Step 3: Grocery Strategy in an Inflation Spike

Switch at least 40% of your grocery cart to store brands — Consumer Reports’ own testing shows they match name-brand quality on staples like pasta, canned goods, and dairy 80% of the time, at 20-35% lower cost.

Meal planning before shopping reduces waste and prevents the inflation tax of impulse buying. Studies show planned shoppers spend 23% less per grocery trip than unplanned shoppers — that gap is even bigger when prices are elevated.

Use cash-back apps like Ibotta, Fetch, and Checkout 51 for every grocery trip. Many offer manufacturer’s coupons stacked with store sales — a combination that can cut 15-20% off your total bill with minimal effort.

Step 4: Protect Your Emergency Fund — Before It Disappears

Many Americans are quietly raiding their emergency savings to cover the gap between income and elevated costs. That is the most dangerous financial decision you can make right now.

Once your emergency fund is gone, the next unexpected expense — a car repair, a medical bill, a job disruption — lands directly on high-interest credit card debt. At current average APRs of 22%, that debt compounds far faster than any gas price decline can fix.

If you’re already dipping in, stop all non-essential spending this month and rebuild a floor of at least $1,000 before resuming normal discretionary spending. Think of it as financial first aid.

Step 5: Review and Renegotiate Fixed Bills

Many Americans don’t realize that car insurance, internet, and subscription services are all negotiable right now — especially as competition for customers has intensified in a slower consumer spending environment.

Call your car insurer and ask about mileage-based discounts — if you’re driving less because of gas prices, you may qualify for a 10-15% premium reduction immediately. For internet and streaming, canceling one premium subscription you rarely use frees $15-20/month with zero lifestyle impact.

Set a calendar reminder for June 1 to review your three most expensive recurring bills. One call per bill — 20 minutes each — can save $50-100 per month. That’s real money in a $4.50 gas world.

The Longer View — How Long Will This Last?

Trump has promised prices will “drop like a rock” when the Iran war ends. That may be true — but nobody can tell you exactly when that happens, and waiting passively is not a financial plan.

Build for six to twelve months of elevated costs, hope for three months, and anything better than that is a gift. The Americans who come out of this period strongest will be the ones who treated the crisis as a long-term planning problem rather than a short-term annoyance.

Disclaimer: This article is for general informational and educational purposes only and does not constitute professional financial, tax, or investment advice. Gas price averages are sourced from AAA as of May 12–15, 2026. Grocery price data is based on BLS CPI April 2026 report. Budget strategies described reflect general financial planning principles — individual results will vary. Readers should consult a qualified financial advisor for personalized guidance based on their specific circumstances.